Spooking the Markets

Pricing panic, adoption reality and the consumer opportunity

If you’re on the go, here’s today’s snapshot:

The reports spooking investors: anxiety vs reality

Where the real tsunami is hitting: software

Downstream question: spillover into other industries?

Reasons to remain optimistic

The Dinner Table Indicator

Last night at a business dinner with many bankers present, the Citrini report (“The 2028 Global Intelligence Crisis” came up again. Like many others we hear Citrini mentioned everywhere. It has gone from a relatively obscure speculative post on Substack to widely quoted almost overnight largely because of its dystopian framing of Agentic AI and labour displacement.

This report, combined with a handful of high profile articles, has contributed to genuine market nerves over the past few weeks. A couple of the key ones are:

Matt Shumer’s Something Big is Happening” argues that current generative AI has crossed a qualitative threshold which will disrupt most screen-based knowledge work.

Dario Amodei’s (Antropic founder and CEO) The Adolescence of Technology where he frames powerful AI as akin to a “country of geniuses” whose autonomy, misuse and indirect impacts could destabilise the world.

Add geopolitical tension and macro uncertainty, and suddenly the mood shifts but the question is a familiar one, are we the start of something structurally different or just another cycle of fear?

Market Anxiety vs. Real Displacement

We are optimistic by nature, but not naive. The anxiety feels real and there has been a genuine market value destruction as investors get cold feet on those industries seen as at risk of margin erosion due to AI such as SaaS. It’s a vivid Illustration that investors are having a hard time pricing AI.

Reuters provides a good example of this volatility. Its share price went down in January on the back of investor doubts, but then went back up again after the CEO showed up in the Anthropic enterprise event (The Briefing: Enterprise Agents), which took place on February 24, 2026.

When we look at the wider economy, however, the scale of actual displacement so far does not match the narrative. Let’s look at some recent examples:

Block

Reports this week suggest roughly 4,000 job cuts, around half its workforce which sounds dramatic but many would argue this reflects over-hiring during the boom years rather than pure AI displacement. As it happened with X. After Elon Musk acquired the company, headcount reportedly dropped from about 6,000 to roughly 1,500 at its lowest point. One of the most dramatic workforce reductions in big tech. But this was a restructuring story as much as a technology story.

Amazon

Around 16,000 corporate roles have been cut in January 2026, but another 14000 were cut last yet. Surely not all is due to Agentic AI, despite the headline.

Pinterest

Pinterest announced 15% job cuts in January 2026 directly due to AI “as it plans to reallocate resources to its artificial intelligence-focused roles and strategy.” However, as Emarketer analyst Jeremy Goldman put it: “Without clear cost savings or a concrete path to AI-driven revenue growth, these cuts look more defensive than strategic.”

In other words: layoffs, yes. Mass AI driven labour collapse, not sure.

Reality Check: AI Adoption Is Still Early

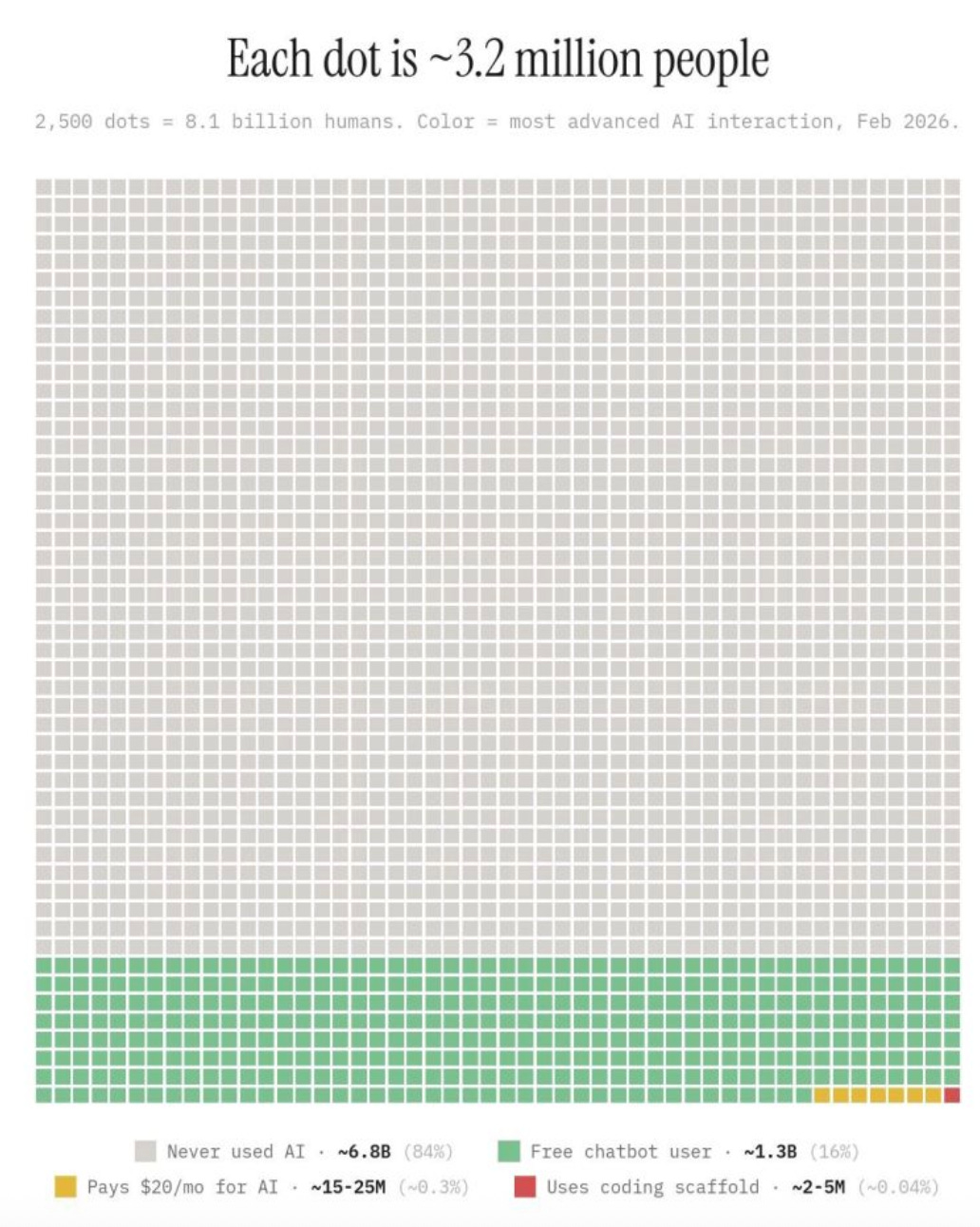

One of the most widely shared visuals from LinkedIn over the past few weeks shows the usage of advanced AI across the global population in blocks of roughly 3.2 million people.

We like it because it is the ultimate reality check of where we stand in terms of AI adoption globally, namely low.

Source: LinkedIn

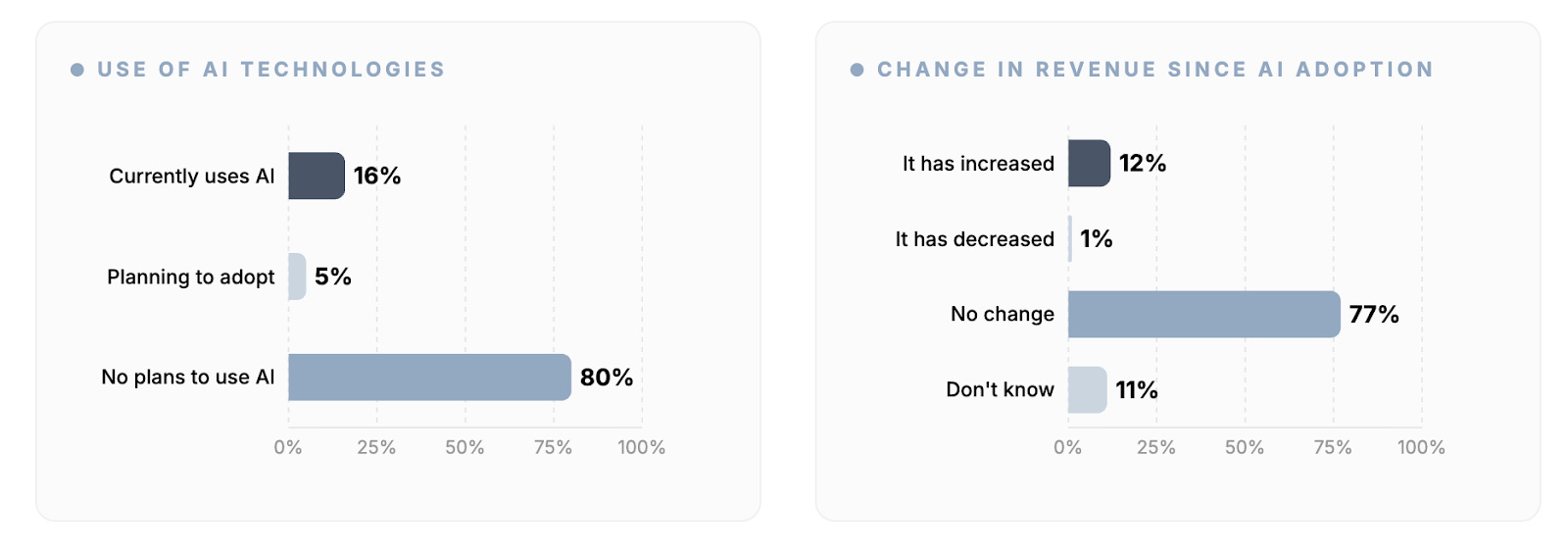

In regards to enterprise adoption, according to UK DSIT, the vast majority of businesses in the UK (80%) neither use nor have plans yet to use AI. Only around 1 in 6 businesses (16%) are currently using at least one AI technology and 5% have plans to adopt AI in the future. Over half of businesses (51%) do not see AI as relevant to their organisation. And only 12% see a revenue increase on the back of AI adoption.

The UK AI Gap: Adoption vs. Revenue Reality

Source: CxAI with data from UK DSIT (Feb 2026)

Where the Tsunami Is Actually Hitting

Now, let’s be clear. The market is not entirely wrong to be concerned about the impact of AI. There is one sector where the tsunami is real - software.

Coding is uniquely suited to AI because:

Code is a structured language

Outputs are testable

Success is binary - it runs or it does not

There is a huge amount of free training data in existing Open Source

That makes it the perfect training ground for agents!

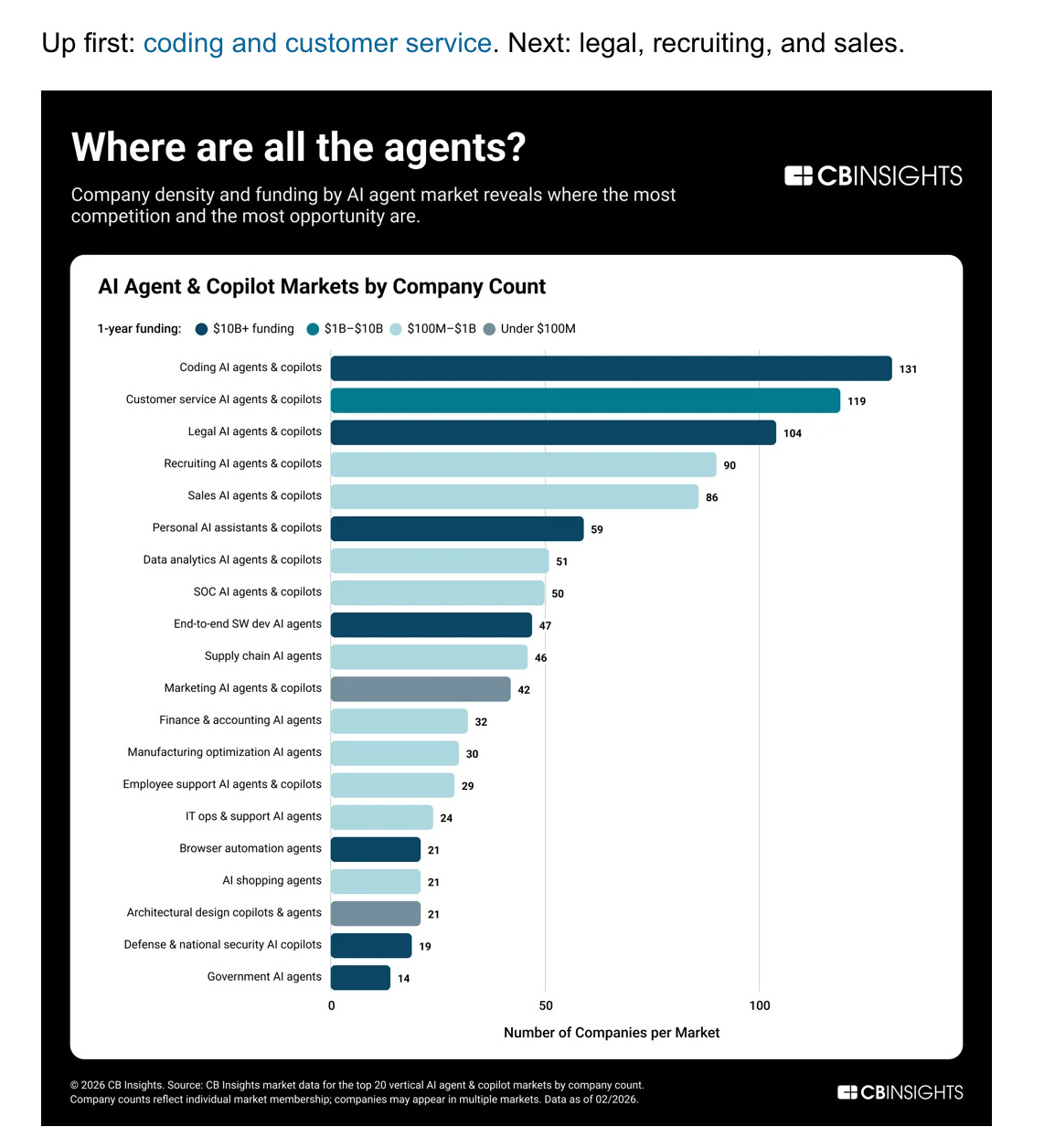

Additionally, CB Insights data from February 2026 below shows AI agent deployment heavily concentrated in software development followed by customer service and legal.

Source: CBInsights

The Downstream Question

The real debate is not whether AI works in coding. It clearly does.

The debate is whether the wave will move downstream of coding into the rest of the economy at the same velocity.

Domains outside of coding tend to be more unstructured, not as easy to test, don’t generate binary answers, and don’t benefit from a large freely available quantity of high quality pre-existing training data.

In addition, while there are no natural breaks in AI capability development, there are natural breaks in economic adoption such as regulation, integration cost, cultural resistance, trust.

The wave will eventually move beyond software. But the panic is premature.

Reasons To Be Optimistic

We believe the opportunity outweighs the threat. Agentic AI dramatically reduces the cost of building digital products. That alone changes the equation for consumer businesses.

You no longer need massive tech teams to ship a product. You can prototype, test and iterate faster than ever. Historically, when production tools become cheaper, innovation increases rather than decreases.

Industrial automation did not eliminate manufacturing. It increased output. Cloud computing did not reduce innovation or the number of startups. It was a force multiplier.

Why would AI be different? If the past 2 years were “software, software, software,” perhaps the next wave is “consumer, consumer, consumer.”

The CxAI Take

Right now, leaders should ignore the noise about immediate job extinction and focus on one question: How does AI make my current business structurally better? The biggest risk today is not displacement. It is inertia.

As Fredrik Cassell at Creandum puts it:

“In this environment, standing still isn’t really an option. The companies that thrive will be the ones willing to rethink how they operate. If you were starting Workday today, you’d build it in a fundamentally different way.”

Stay tuned for our upcoming deep dive in partnership with Anna Shipman.

And as always, feel free to send us your feedback or suggestions for future posts, we love them!

Your CxAI team

Note: If you know Cambridge you will hopefully like this reference!

Good article! Two cents:

Coding is highly suited to AI for the reasons you mention, but there are usually many ways to reach the same outcome in software. AI’s usefulness depends on how well we specify both “what” should be built and “how”to get there, to maintain quality of the asset. The bottleneck shifts from execution to specification, which itself is a meaningful change in the SDLC.

More broadly, standing still has never been a viable business strategy. Nokia saw Symbian’s limits before the iPhone launched; engineers raised the concerns, but the company protected short-term roadmaps and margins instead of acting. We could conclude the winners will be businesses that combine strong frontline information flow with AI-enabled speed in accommodating the needed changes.